The Return of Geopolitics

If recent years and particularly the last six months have taught investors anything, it is that geopolitics cannot be ignored.

Conflicts, supply-chain realignment, energy security and changing trade relationships have all played a more prominent role in markets than many would have anticipated a decade ago. Governments around the world are increasingly prioritising resilience and security over efficiency alone. While this creates uncertainty, it is also generating interesting investment opportunities in infrastructure, defence, energy networks and advanced manufacturing.

The challenge for investors is avoiding the temptation to react emotionally to every headline. As we have noted previously, history consistently demonstrates that geopolitical events often have a much shorter impact on long-term market returns than investors initially fear. The discipline to remain invested through periods of uncertainty has repeatedly proven valuable.

A Warsh led Fed

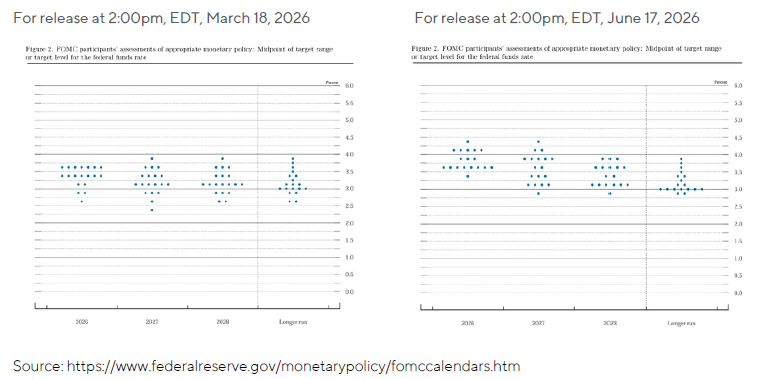

Something that caught our eye over the last month was changes to the dot plot provided by the Federal Reserve (Fed) in the US. For clarity, the dot plot is a chart published by the Fed after certain meetings that shows where each policymaker expects interest rates to be at the end of the next few years. Each "dot" represents the view of an individual policymaker, with the median dot often viewed by markets as the best indication of the Committee's likely policy path. While it is not a promise of future action, investors closely watch changes in the dot plot because they can signal whether the Fed is becoming more hawkish (favouring higher rates) or more dovish (favouring lower rates).

As seen from the above, there was a notable move up in the dots, particularly in 2026. The interpretation of this is that the expectations for 2026 moved from interest rate cuts (lower rates) to interest rate hikes (higher rates), largely reflecting the possible inflationary effects of the conflict in the Middle East.

While investors are focused on the more hawkish signal from the dot plot, there is reason to believe that the Committee may be less hawkish than the headline reaction suggests. With year end inflation expectation being raised, this gives flexibility for the Fed to lower expected interest rates later this year should the impact of the Middle East conflict be less severe than anticipated.

Looking Ahead to the Second Half

As we enter the second half of 2026, our outlook remains cautiously constructive although we should expect volatile periods to persist.

Global economic growth continues to be supported by healthy corporate balance sheets, resilient consumers (with European and Asian savings rates much stronger than US) and substantial investment in technology and infrastructure. Earnings growth remains positive and, importantly, is becoming more widely distributed across sectors and regions.

Inflation remains somewhat sticky in several major economies and central banks may prove slower to reduce interest rates than many had hoped but this is mostly priced into the current yield levels as markets look ahead. Government borrowing levels remain elevated, while political developments on both sides of the Atlantic will continue to attract attention.

The biggest risk facing investors today may not be inflation, elections or geopolitics. It may be the assumption that the future will look exactly like the past. For these reasons, selectivity remains crucial. We believe portfolios should remain diversified across regions, asset classes and investment styles, recognising that leadership may continue to rotate more frequently than investors have become accustomed to during the last decade.

The Great Broadening

For several years, investment returns were concentrated in a handful of exceptionally large US technology companies. While those businesses remain immensely important, investors have increasingly looked elsewhere for opportunities (this was evidenced strongly by the last few months of 2025 and first two months of 2026). Asian technology manufacturers, European industrial leaders, emerging markets and selected UK companies have all begun attracting greater attention. This has been particularly encouraging for active investors, as a broader market environment tends to create a richer opportunity set than one dominated by a small group of stocks.

Liam Goodbrand, Investment Director

9 July 2026

Keep Informed

Sign up to our View from the Square.